Hello, I am an American Adult and I have a Money Problem. No matter that I'm not the only one - I'm just tired of being in debt and living pay check to pay check, and I've made a commitment to myself that I'm going to get this under control. I want to be out of debt by 2016 (I don't mean Mortgage-Free, but everything else). That would give me two or three years to establish a personal savings and get ready to start paying for my kids to go to college.

But big money goals turn out to be made up of lots of small decisions. Sure, there are big decisions, but we've mostly made those and can't really change very many of them (house we bought, car, student loans, etc.). So I'm trying to work with the living budget.

We had previously done a really tight budget with LOTS of categories. I found it impossible to stick to. Life never really matched those categories we had established, and we'd start by trying to shift funds about and then when it got too complicated we would just bag it all and let the budget fail.

The process was going to have to be simpler and more flexible if we were going to stick with it.

At the start of this calendar year, I tried something new. I sat down and did something very simple: I took our total monthly income and just subtracted all the fixed bills and expenses from it. In that first go-through, I didn't evaluate any of those expenses, I just laid them out as a given.

The magical result of that simple exercise was how much money we had left for non-fixed expenses. Conveniently, this turned out to be a round number well-suited to be divided three-ways for

1. Food (both groceries and eating out)

2. Credit Card payments

3. Everything Else

That last category is the sticky-wicket (what does that even mean? I digress).

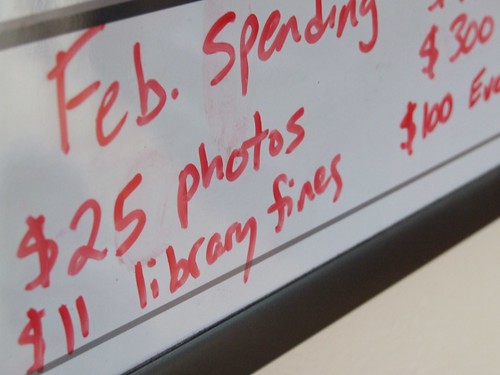

To keep track of our spending in the "Everything Else" category we have started writing the Big Number on the kitchen whiteboard at the beginning of the month, then writing down every expenditure and subtracting it so the total keeps changing to say "$ Left". That big "$200 Left" or whatever is a real wake-up call when we see it right there.

It's right out there where we (and anyone else visiting our home) can see it. I'm trying to break the acculturation that says I can't talk about money and need to just always act like I have plenty of it (even if I don't). That's part of what got us into debt in the first place.

It's working better than anything else we've tried. There are still many challenges, but I have some hope that six months from now I'll be able to report progress.

I'm inspired to see more people talking honestly about money and debt. This post at Simple Kids is an example. There are plenty of people like me out there, trying to get it under control.

Budgeting is tough. I applaud you for writing it all down on the whiteboard! That would be incredibly hard for me and husband. It is the nickel and dime stuff that sends us over the edge. I have to chuckle (in a friendly way) at your library fine. Ours are routinely over $40 bucks. Obviously something we can control, but somehow just can't manage!! Why!?! I wish you the best of luck. People do need to be honest with what they can and can not afford.

ReplyDeleteSo much truth here. And I agree with Plaid Shoes, it's the little stuff that kills us. A few months ago we started using a spend tracking app and I began couponing and shopping sales in earnest. I always thought couponing would be a waste for me, that it would mean buying a bunch of junk, but I've found extra savings on produce and staples like canned beans and GF pasta. It's helped tremendously, shaving 30-50% off our weekly bill. We often wonder where everyone gets all their money from as well....

ReplyDelete